CARES Act passed March 27, 2020

The $2 trillion CARES Act passed March 27, 2020, and it is essential for small business chiropractors to understand the Paycheck Protection Program section of this bill. Chiropractic care needs to support it’s communities now more than ever. The passing of the CARES Act should not only help chiropractors weather this turbulent pandemic but help their employees as well with the Paycheck Protection Program.

Below is a summary of this Chiropractic F.A.Q.Guide to the Coronavirus Relief Bill. Keep scrolling for a detailed overview of each fact or question. We will continue to update this post and the Dr. Nick Facebook Page with more interviews from key chiropractic industry experts as more information unfolds, so make sure you are visiting this page often.

What is the Paycheck Protection Program?

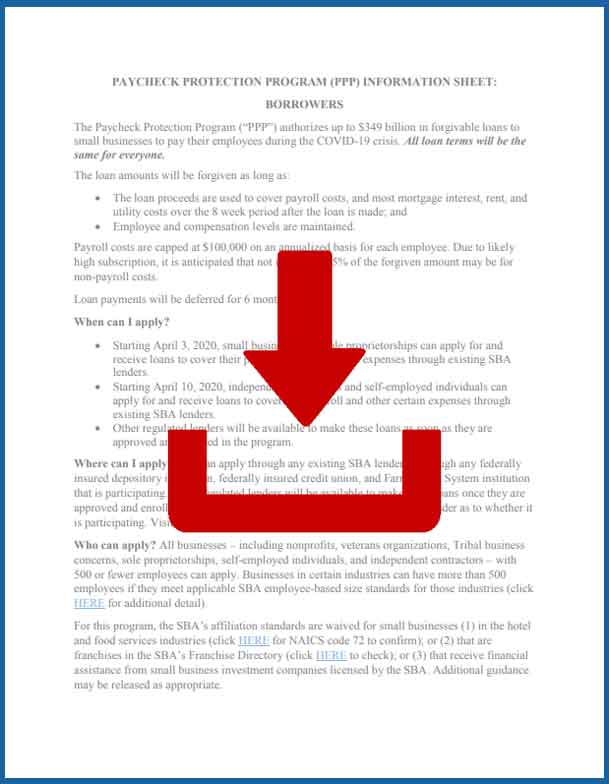

This lifeline program intends to act as partial revenue replacement for affected small businesses with under 500 employees – the majority of chiropractic offices.

Are all chiropractors eligible for Paycheck Protection Program?

Most should be. Any business with less than 500 employees and classified as sole proprietors, self-employed individuals, or independent contractors.

What is the max loan amount I will be able to borrow?

The maximum amount available for chiropractors will be 2.5 of the average monthly payroll cost incurred over the prior 12 months from that date that you apply for the loan (not to exceed $10 million). If you have been in business for less than one year, they will use your payroll information starting 1/1 to 2/15.

What can this loan be used for?

Payroll costs including employee salaries and health care benefits, interest on a mortgage, rent, utilities, interest on any debt incurred before February 15, 2020

Where can I obtain a loan under the Paycheck Protection Program?

Chiropractors will be able to apply for this loan at any SBA-certified lender (over 1,800 currently), and probably most FDIC insured financial institutions.

Is it difficult to apply for a loan under the Paycheck Protection Program?

It definitely won’t be as difficult as the normal SBA loan process. According to recent reports, the process should be fairly streamlined.

What are the requirements to apply for a loan under the Paycheck Protection Program?

Documentation that you were in business before February 15, 2020, and that you were paying people before February 15, 2020. That includes yourself if you are a solo-practitioner or contracted doctor. Also, the borrower must certify that you are not receiving funds for the same uses from another SBA lender.

Is a loan under the Paycheck Protection Program forgivable?

Yes. But only if the borrower meets specific terms

(UPDATE 4/3) I Finished My Paycheck Protection Program Application And Here’s How I Calculated My Average Monthly Payroll And What Documents I Submitted

Paycheck Protection Program Borrower Fact Sheet Download

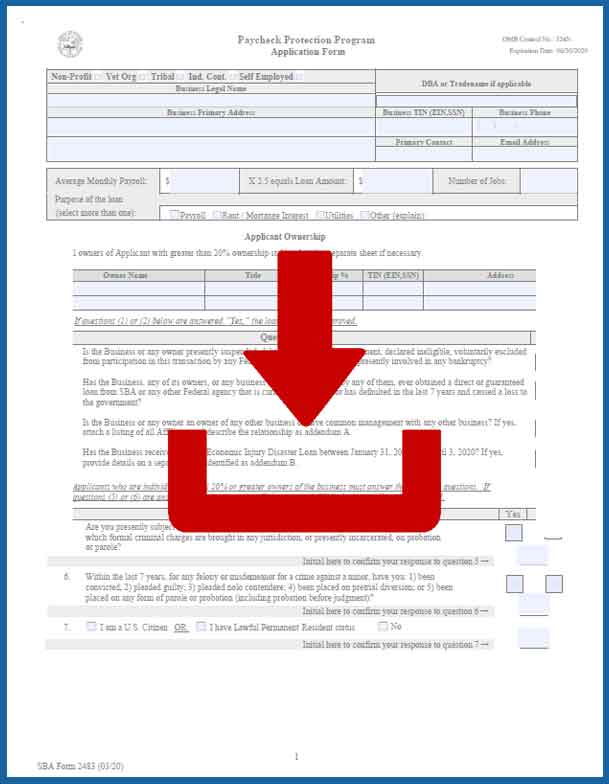

Offical Paycheck Protection Program Loan Application Download

Here's A Brief Video Breakdown Of What The Paycheck Protection Program Will Mean For Chiropractors If You Don't Have Time To Read This Whole Post

What is the Paycheck Protection Program (PPP)?

This lifeline program intends to act as partial revenue replacement for affected small businesses with under 500 employees which I would imagine would be every Chiropractor in business for themselves.

How does the PPP work?

Under the Paycheck Protection Program, chiropractors will be able to apply for a forgivable loan to cover specific operating expenses, particularly payroll expenses, at any SBA-certified lender (over 1,800 currently). The maximum amount available for chiropractors will be equal to 2.5X of the average monthly payroll cost incurred in the 12 months prior to applying for the loan (not to exceed $10 million).

Payroll costs covered will be wages, salaries, retirement benefits, healthcare, sick leave, vacation, and other broadly defined payroll incurred bills under the Paycheck Protection Program. Other covered categories will include rent, utilities, interest on your commercial mortgage, and interest on your business loan(s).

The program will provide a six month to 1 year grace period for repayment, and what’s critical here is that chiropractors who do borrow under this program will be eligible for loan forgiveness equal to the sum spent on covered expenses during the 8-week period from which the loan originated from. So that means if you follow all of the requirements the loan may be 100% forgiven. If it is not totally forgiven the non-forgiven portion will turn into a loan with generous repayment terms.

To get the full benefit of loan forgiveness, businesses must keep employees and pay them at least 75% of what they were making before all of this hit. If you have already had to lay off employees at your practice, you would be able to bring them back onto the payroll. This bill is retroactive to February 15, 2020, so if you did have to lay someone off after February 15, you could hire them back to your practice, and their payroll will still be covered under this program.

What Do The Covered Expenses Include For PPP?

What Expenses Are Not Included In PPP?

In addition, the CARES Act will be sending $1,200 stimulus checks to employees who make under $75,000 per year. This check will either be directly deposited or mailed depending on how the employee files their taxes.

Both the loan forgiveness program and stimulus checks are a tremendous positive for chiropractic offices because it will allow teams to stay together. If patient numbers are lower than average, now might be a great time to start working on projects you have wanted to work on but just haven’t had time for. Because the majority of Americans are at home online right now, we highly suggest amping up your digital marketing strategy.

We suggest going through the Chiropractor’s 2020 Marketing Guide we put together on our blog. Tips on how to shoot engaging video, blogging, podcasting, and more are shared there.

What Is The Eligibility Period For The PPP?

From February 15, 2020 until June 30, 2020.

What Documentation Is Needed To Apply For PPP?

The process to apply for a Paycheck Protection Program loan is supposed to be straightforward and simple. Your SBA-certified lender will need to verify that the business was in operation before February 15, 2020, and paid employee salaries and payroll taxes or independent contractors.

For more information on exactly what documentation is needed and to start the application process, it is strongly recommended to contact a personal banker and schedule an appointment as soon as possible. It can be guaranteed that the line of applications for a PPP loan will be quite long.

How Will The Loan Amount Be Calculated?

The Paycheck Protection Program is calculated from the last 12 months of your payroll. It will be 2.5X your average monthly payroll expenses. Payroll costs will include your regular salaries, taxes, retirement, health insurance, and more.

The Paycheck Protection Program is created to keep you paying your employees. Watch the video for way more detail on how it is calculated.

What Chiropractors are eligible to apply for the PPP loans?

It is simple. All Chiropractors that are self-employed, have under 500 employees, in business before February 15th, 2020 and paying employees by then will be eligible to apply. Don’t worry, if you are a Chiropractor and are the only one working in your practice, you qualify too!

It is important to know if you qualify. Watch the video for more details.

How will Chiropractors apply for the PPP loans?

The SBA is still giving guidance (as of 3/30) to the local banks and credit unions. Banks will be providing the loans directly though. If you don’t have a banker, I highly suggest getting one now to be prepared.

For now, make sure you have the last 12 months of payroll documents ready for when more information becomes available. Watch the video for way more detail and check out my video on what documentation you will need too!

What will payroll costs be defined as for Chiropractors?

The Paycheck Protection Program is going to help cover costs a ton. When it comes down to payroll it is up to $100,000 of payroll cost prorated over 8 weeks. Plus, this will cover vacation, sick leave, severance pay and much more. Basically anything in terms of pay or benefits that you spent money on in the past 12 months will be covered by the Paycheck Protection Program. Watch the video to learn more.

How long will it take for Chiropractors to get this money?

As soon as the money is available from SBA the banks will begin distributing it. The government has been saying that you’d be able to get money the same day the loan originated, which may also be the same day you apply for the loan.

The approval will be much simpler than a normal loan making this fast turnaround possible. Making sure you are prepared is a good plan to have so you can get the money as fast as possible to help your practice. Watch the video for way more detail.

What portion of these loans will be forgiven for Chiropractors?

The portion of the loan that is used for covered categories up to 100% of the loan amount. The covered categories include payroll, healthcare benefits and insurance premiums, salaries and commission/compensation, mortgage, rent, utilities, and interest on debt obligations.

There are some things you have to abide by to get 100% loan forgiveness. Watch the video for more detail, what isn’t covered and how to make the most of the loan.

Should a Chiropractor hire someone to do their loan application?

As a Chiropractor or just a small business owner, the simple answer is – no. They are trying to make this process as simple as possible. The application process will be easy if you have the documents you need. Work with the bank where your business checking is at first. Watch the video for way more details on why Chiropractors should not have someone help do the application.

Is this money for Chiropractors a loan or a grant?

The Paycheck Protection Program money is a loan that may be forgiven at the end of the 8 weeks. But, to have it 100% forgiven you have to follow the rules. If you don’t, it will turn into a loan you have to pay back at up to 4% interest and up to a 10 year repayment plan. Watch the video for more information.

How will Chiropractors qualify for loan forgiveness?

For Chiropractors to qualify for loan forgiveness, you will need to show proof that you spent the loan money on covered categories. Please see the covered categories at the beginning of the blog. At the end of the 8 weeks, you will apply for loan forgiveness. If you followed the rules, it should be easy for you as a Chiropractor to be granted loan forgiveness. Watch the video for way more details.

What should Chiropractors say to their bank about this program so they know what they are talking about?

At this point in time it is best to just be as straight forward as possible and not ask too many questions, as they may not have the answers. To set up an appointment, tell your banker you want to apply for the Paycheck Protection Program loan program. Not the EIDL. Watch the video for a full example of what to say when you speak to your banker about the Paycheck Protection Program.

When this loan is forgiven for Chiropractors will it be counted as income on their income taxes?

This loan will not be counted as income on your income tax. This is written in the bill. Once it is forgiven, it is like it never happened. This loan is made to help you as much as possible. Watch this video and the others for more information.

What happens if a portion of the loan is not forgiven at the end of the 8 weeks?

If you use this money for non-covered categories (which I highly suggest not doing that) the loan will turn into a regular loan. You should be able to differ the payments for a few months to help get back on your feet though.

This loan is made to help you, use it wisely and make sure you know all of the details so 100% will be forgiven at the end. Watch the video for way more detail.

What are the covered categories Chiropractors can use the money for?

The covered period began on February 15, 2020. The covered categories are as followed: Payroll, Group Healthcare Benefits and Insurance Premiums, Salaries/Commissions and Compensations, Mortgage Obligations,Rent and Rent Under A Lease Agreement,Utilities, an Interest on Debt Obligations. With Payroll it is up to $100,000 a year/pro-rated from 8 week and includes sick time, vacation time, severance pay and more. Watch the video for more details and what is NOT included.

What type of documentation should Chiropractors get together for this program?

All of your payroll costs for the past 12 months and anything a bank would normally ask for when applying for a loan (even though you may not need it all). What that looks like is – your tax returns, year to date numbers, personal financial statement and your accounts receivables aging report. I go through a full list in detail in the video. Make sure to watch!

Can Chiropractors Get Economic Injury Disaster Loans Through The SBA AND Take Advantage Of The Paycheck Protection Program?

A disaster loan is typically for natural disasters but since COVID-19 has been marked as that, businesses were able to take out the loan. Now, people are wondering if they can get the Paycheck Protection Program loan as well. It may seem complicated but the short answer is yes, IF you took the disaster loan out before the Paycheck Protection Program loan becomes available.

In this video I go into how you can do both and when you can’t. Watch the video for more information.

A couple of big updates for sole proprietor Chiropractors concerning unemployment and calculating your payroll costs.

You MAY be able to use things like Schedule C’s, K1s, tax returns, etc. to prove your own pay. Self-employed people will also be able to file for unemployment now. Most importantly, have more documents than necessary to show proof. Watch the video for more details on self-employment and unemployment. This is a huge question being answered.

IMPORTANT FOR PEOPLE WONDERING ABOUT DISTRIBUTIONS!

I reread the bill. Here is exactly what it says about documentation needed for sole proprietorship’s, IC’s etc. This includes payroll tax filing, forms 109-MISC, and income and expenses from the sole proprietor as determined by the administrator and secretary. This statement encompasses almost any practice a Chiropractor could have.

For more information watch this video, there is a lot more detail to hear.

SBA Disaster Loan AND PPP Loan? I reread the bill. Here is what it says about that.

You can get the Disaster loan and the PPP loan, BUT it can’t be for the same categories. Meaning, there can not be any overlap. If you get the Disaster loan for payroll, you can’t use the PPP loan for that as well. SO, I suggest if you have the Disaster loan, use it for categories that are not covered by the PPP loan. But watch the video for the details as I reread the section on this.

Who gets priorty for a Paycheck Protection Program Loan?

With the Paycheck Protection Program there are those that will get priority. If you are in an under-served or rural market, a veteran or a member of the military community, a minority or female-owned business or a business in operation for less than 2 years you should get priority. Watch the video for the details as I reread this portion of the bill.

What if I own my building through an LLC and my Chiropractic office pays rent to the LLC? And what qualifies as a "covered mortgage obligation"?

A covered mortgage obligation means any indebtedness or debt instrument incurred in the ordinary course of business that (a) is a liability of the borrower, (b) is a mortgage of real of personal property, and (c) was incurred before February 15, 2020. So if you own it, and LLC owns it or the business owns it – it is covered. Watch the video for details.

I reread the bill and here is what it says qualifies as a utility in the covered categories. It's GOOD news!

Good news! With the Paycheck Protection Program, utilities are under the covered categories. Now, a big question is what does that mean? It means -electrical, gas, water, phone, internet and transportation all are covered if you so choose to use the loan for those expenses. Watch the video for the details.

Loan Forgiveness Reduction based on reduction in NUMBER of employees. This is a big one.

You can’t get forgiveness over what you borrowed. But you get to choose either them calculating the average number of full time equivalent employees from February 15, 2019-June 30th, 2019 or from January 1st, 2020 – February 29th-2020. Watch the video for the details and a better explanation.

What to do with people you have already laid off.

Most popular question talked about here. I reread the section of the bill regarding if someone has laid employees off. The bill gives two circumstances that we take a look at. From my understanding, you will need to bring your employees back if you have laid any off by April 27th. Watch the video for the details and more in-depth discussion.

Will this money that is forgiven be counted as taxable income?

The Paycheck Protection program was created to help. Once the loan has been forgiven it will not be counted as taxable income. It will be as if it never happened. Plain and simple. Watch this video and others for more questions answered regarding the Paycheck Protection Program for Chiropractors.

More language from the bill about PPP loans and Disaster Loans.

With this tax credit, you aren’t able to get special SBA loans with it. Double check if you want to use this for your first quarter. Run your numbers and read the fine print. It may not be compatible with the Disaster loan or the Paycheck Protection Program. Watch the video for the details.

When will they decide if your loan can be forgiven or not?

At the end of the 8 weeks, you will apply for forgiveness. You will be notified no longer than 60 days on the loan forgiveness decision. Watch this video and others for more information. In another video I suggest how to be sure you get loan forgiveness.

Emergency EIDL Grants and what the bill says about them.

As I understand the grants, if you applied for the Disaster loan, you can request up to $10,000 grant. With the EIDL Grant they use your credit score and alternative methods. If you don’t get the loan, you still get the grant. Watch the video for more details and explanations.

Section from the bill that says the SBA will PAY FOR your SBA loans for the next 6 months.

Not only will they pay for the interest but they will pay for the principal for the next 6 months. And if you have something on deferment, it will pay the next 6 months. And more! Watch the video for more explanation and details.

Unemployment options for the self-employed Chiropractor.

Usually if you are self-employed, you cannot go on unemployment. But this bill changed it and extends the typical length for unemployment as well. This will allow $600 extra each week on top of what your state will pay for unemployment. So, if you can’t show you have been paying yourself or are collecting a loss – this is a good option for you. Watch this video for more information.

What my bank's SBA specialist says you should do now if you haven't applied for a PPP loan yet.

The best thing you can do is call your bank and make an appointment. Friday 4/3/2020 is the deadline the SBA have been given to get the information to the banks. It is important to be, or try to be, first in line with your bank. Watch this video and other for the details on how to be prepared.

What my commercial banker told me about PPP documentation.

Have your payroll calculations ready, as well as your updated financials per my banker. Have more than what you need and get your normal documents you would need for a normal loan. Get it done fast, to be at the front of the line. If bankers want more, give it to them. Watch the video for the details.

Be VERY careful with the tax credit incentivizing the maintaining of your payroll (this is different than the Paycheck Protection Program)

In this bill it says you can’t use the Disaster loan and the Paycheck Protection Program “for the same purpose”. “For the same purpose” is the key term. Meaning you can’t get both for your payroll. There needs to be more clarification on this but for now this is my understanding from the information provided. Watch the video for more of an explanation.

A four-part dive into your questions about the Paycheck Protection Program for chiropractors...

In addition, I broke a #AskDrNick weekly episode into four episodes to give you all the best information with no time frame! In this episode, I covered questions like…

Owning your own practice with no staff, what are my options?

To…

How much should I apply for the SBA loan?

Watch all four episodes below.

Also, I compiled all of the videos included in this post into a Senate CARES Act – Paycheck Protection Program Explained YouTube Playlist on my Dr. Nick Channel dedicated to smart business advice for chiropractors. Feel free to share so we can help out as many chiropractors as possible!

Here is the latest Q&A I streamed on the Paycheck Protection Program Treasury Document that details necessary information regarding loan applications.

What does this mean for the future of chiropractic care?

Now more than ever, the world understands the importance of immunity towards viruses and infectious diseases. Chiropractic care is the key to increasing the central nervous system’s health and helping our body’s immune system perform at a higher level. Let’s share this message with the world!

Chiropractors need to take advantage of this opportunity to reach families who are stuck at home with content online that is engaging and educational. We truly are all in this together, and chiropractic care will come out stronger on the other side of this pandemic.

If you have any additional questions about the Paycheck Protection Program and how it pertains to your practice, our team is here to help.

Stay Safe & Healthy Doc –

Dr. Nick

drnick@lvrgmedia.com